Homeownership creates long-term stability and gives people the opportunity to build equity over time. It is also one of the most significant financial decisions most people will make, especially on the Central Coast, where high property values require thoughtful planning and the right financing strategy. For buyers and homeowners, American Riviera Bank exists as a local financial partner that helps with preparation, understanding available lending options, and understanding the market.

Owning a home can create financial flexibility through equity growth, appreciation, and access to lending tools that support future goals. For many homeowners, equity becomes a resource that helps fund renovations, support life transitions, or provide financing for the next property purchase.

Buying a home should always align with your financial reality. Strong homeownership decisions begin with a clear understanding of what you can comfortably afford and what ownership requires beyond the purchase price.

For many Central Coast buyers, saving for a down payment is the biggest obstacle to purchasing a home. Grant programs available through American Riviera Bank are helping address that challenge.

As a participating lender with the Federal Home Loan Bank of San Francisco, American Riviera Bank offers access to two grant programs designed to help first-time buyers bridge the gap to homeownership.

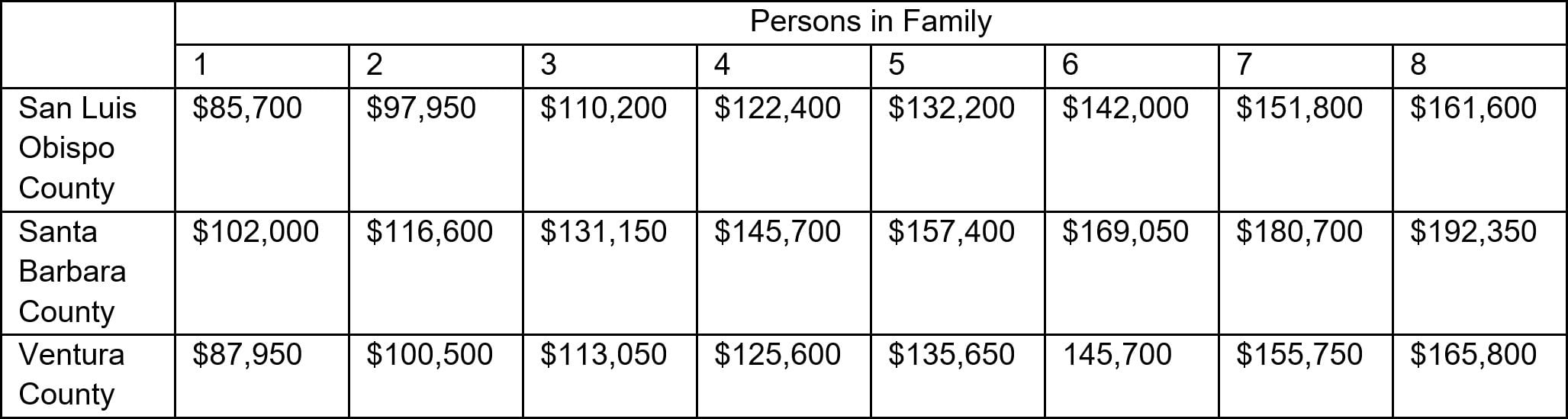

The Middle-Income Downpayment Assistance Program (MDPA) provides eligible first-time buyers with grants of up to $50,000 for down payment and closing costs. Earlier this year, the program’s first round of funding totaled $8 million in March 2026, and a second round of $3 million is expected to open later this year.

This program is designed for households earning between 80.01 percent and 140 percent of area median income, depending on household size and property location. It is especially valuable for middle income professionals who often earn too much to qualify for traditional assistance programs but still face barriers to purchasing in high-cost markets.

Funds are grants, not loans, and do not require repayment or a forgiveness period.

Eligible borrowers must complete homebuyer education, contribute at least $10,000 toward the purchase, and purchase an eligible primary residence.

Additionally, the Workforce Initiative Subsidy for Homeownership, or WISH Program, is currently live and supports low to moderate income first-time buyers with 4-to-1 matching grants of up to $32,837 in 2026.

WISH funds can be applied toward down payment and closing costs and may be combined with other local, state, and federal homeownership programs.

To qualify, buyers must meet income eligibility requirements, complete homebuyer counseling, contribute toward the purchase through savings or approved matching contributions, and purchase an eligible owner-occupied property.

* Eligibility requires meeting program guidelines at the time of enrollment, including having a household income at or below 80% of the U.S. Department of Housing and Urban Development (HUD) Area Median Income.

Both programs are available on a first-come, first-served basis, making early prequalification essential. For qualified buyers, these grants can significantly reduce the upfront cash needed to purchase a home.

As equity builds, homeowners gain access to financing options that can support future goals.

Home Equity Loans provide a fixed amount of funding with predictable monthly payments. These are often well suited for planned expenses such as renovations or debt consolidation.

Home Equity Lines of Credit offer revolving access to available equity, which can help cover ongoing projects or unexpected home expenses.

The right option depends on how and when funds will be used.

For current homeowners, timing the sale of one property while purchasing another can be challenging. Luckily, there are options available to make the process easier, such as a bridge loan or a concurrent loan closing.

Bridge loans can provide short-term financing that allows buyers to secure a new property before selling their current home.

Concurrent closings offer another option, allowing both transactions to happen at the same time and reducing temporary financing needs.

The best structure depends on your timeline, available equity, and market conditions.

In certain scenarios, building a home can offer more flexibility than purchasing an existing property. This is where American Riviera Bank steps in to help with residential construction loans.

Lenders typically require a complete project plan that clearly outlines what will be built and how the project will move forward from start to finish, such as contractor documentation, realistic budgets, and a lender review of project feasibility.

Gathering these details early on helps demonstrate your commitment to the project while keeping the process efficient and expectations clear.

Real estate decisions are rarely one size fits all, especially on the Central Coast. National Homeownership Month is a good time to review your financial position, explore available assistance programs, and evaluate your options with a local lending expert.

Whether you are purchasing your first home, using equity to improve your current property, building from the ground up, or exploring grant opportunities through MDPA or WISH, American Riviera Bank’s Residential Lending team can help you assess eligibility and structure a plan that fits your goals.

Get started today by connecting with a local lending specialist to explore your options and find a loan that fits your financial situation.

Member FDIC | Equal Housing Lender | NMLSR#808293

Previous: 2026 Graduation Next: Dog Day 2026